In a bid to reduce monthly outgoings, first-time buyers are increasingly choosing mortgages with longer terms. While this can be a useful strategy, the amount of interest paid over the full term will be much more. If you’re thinking about taking out a longer mortgage, you should consider the long-term impact too.

Rising house prices mean it’s increasingly difficult for first-time buyers to step onto the property ladder. Not only do you need to save more for a deposit, but repayments will be higher too. Average house prices increased by 7.1% in the year to August 2021, according to Halifax. So, it’s not surprising that first-time buyers are looking for ways to make paying a mortgage more affordable.

The rise of 35-year mortgages

Traditionally, a first-time buyer would take out a mortgage over 25 years. However, as house prices have increased, the number of first-time buyers opting for longer-term mortgages has risen.

According to research conducted by Quilter, there has been a 70% increase in mortgages with a term of 35 years or more between March 2019 and the beginning of 2021. While this can make repayments more affordable, it could mean you spend far more on interest payments over the full term.

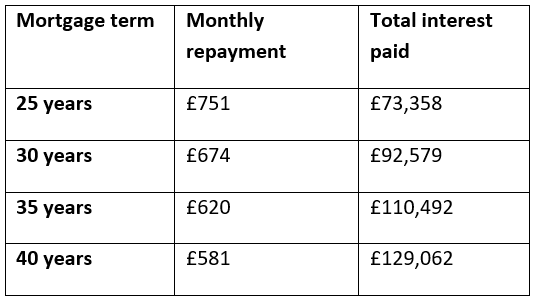

The table below shows how monthly repayments and total interest change depending on the mortgage term for a £150,000 repayment mortgage with an interest rate of 3.5%.

Source: Money Saving Expert

In this scenario, switching from a 25-year mortgage to a 40-year mortgage means your monthly repayments fall by £170. That can make paying a mortgage more affordable or provide a buffer in your budget to cover unexpected costs.

However, when you look at the total interest paid, is it worth it? Choosing to take out a 40-year mortgage would mean you pay an extra £55,704 in interest over the full term. If you have the means to, choosing a shorter mortgage term makes financial sense in the long run.

It’s not just the interest payments you need to consider either, but the impact on your lifestyle. With the average first-time buyer in the UK now in their 30s, a 40-year mortgage could mean you’re in your 70s before you pay it off. That could affect your retirement plans or mean you don’t have the flexibility you want.

When taking out a mortgage, you should consider your needs now and those in the future to ensure you pick the right option for you.

While a shorter mortgage term can save you money in the long run, it may not be an option as a first-time buyer, but there are other steps you can take to reduce the bill over the full term.

3 ways you can reduce interest payments over the term of your mortgage

1. Make overpayments

If you want to pay off more of your mortgage each month without committing, overpayments can work.

When you overpay your mortgage, this amount is taken directly off the amount you owe, rather than covering interest payments. As a result, even small, regular overpayments can reduce the amount of interest you pay over the long term. You can usually choose whether to make regular overpayments or lump sums.

One thing to keep in mind is potential charges. Usually, you can overpay up to 10% of the remaining balance each year without incurring charges. However, you should always check the terms of your mortgage before making an overpayment to ensure you don’t incur unexcepted fees.

If you plan to make overpayments, it’s worth factoring this into your decision when looking for a mortgage. If you’d like support, please contact us.

2. Reduce the mortgage term at a later date

Just because you opt for a longer-term mortgage initially, doesn’t mean you need to stick with this time frame. When a mortgage deal runs out, you can choose to remortgage with a shorter mortgage term. For instance, you may initially take out a 40-year mortgage with a 5-year deal, and when this runs out choose a 25-year mortgage to reduce the full term by 5 years.

This means that as your financial situation changes, you can adjust the mortgage term to suit you. Many first-time buyers will find their income increases, so shorter-term mortgages will become more affordable. Reducing the term where possible could save you money.

3. Remortgage when your mortgage deal runs out

While you may take out a mortgage with a 40-year term, your initial deal is likely to last for two, three, or five years. When this deal runs out, you will usually be moved on to your lender’s standard variable rate (SVR) to calculate interest. In most cases, this rate is not competitive and will mean your interest rate is higher than necessary.

Make sure you note when your mortgage deal runs out, and look at what your remortgaging options are. Even a small reduction in the interest rate could save you money in both the short and long term.

If you’re ready to apply for a mortgage, whether as a first-time buyer or to remortgage, we’re here to help you secure the best deal for you. Please contact us to discuss your needs and goals.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

Production

Production